When you eat a heavy meal, it can often make you feel sluggish afterward and even disrupt sleep. But getting up and taking a short walk after eating can help combat this. Not only is walking a great low-impact activity to help you stay healthy overall, it can specifically aid digestion and control ... Read more

March 2019 Newsletter

Dear Esteemed Clients and Friends,

We hope 2019 has started well for you all and hope it continues to be a good year, both from a family as well as a financial perspective.

I had recently attended the annual Chief Economists’ Forum in Sydney and thought I would share some highlights with you.

Despite expectations of a US recession sometime within the next couple of years, US growth seems to be continuing with continued wage growth acceleration and a robust US labour market. Consensus view is that the US will remain on hold with regards to interest rates in 2019 and the view is quite similar for Australia with a slight skew now towards a rate cut.

Global growth slowed in 2018 and it’s still decelerating. China fell sharply but may pick up by mid-year, assuming the US/China trade issues are somewhat resolved. European manufacturing activity remains weak as industrial output declined three of the last four months. This signals contraction. The services side of the Eurozone economy, however, is better. Consumer confidence fell but remains mostly solid, likely because the labour market is holding up well. This solid job news is broad-based throughout the Euro area. The European Central Bank will stay accommodative, likely changing its guidance to no rate hikes this year and restarting its bank lending program. China’s fiscal stimulus may boost global trade in the second half, supporting Eurozone exports and manufacturing. In Japan, the expansion continues. Japan is part of the global supply chain that’s being disrupted by the trade dispute between the U.S. and China. U.S. auto tariffs loom for Japan and Europe as well. The labour market remains a bright spot with an incredibly low jobless rate of 2.5%. The ratio of job openings to the number of applicants is 1.63, around the highest since 1974, so there are plenty jobs for workers. However, the growth risk is likely on the downside; retail sales are struggling and a drop in profits may impact capital spending.

Activity in China may be stabilizing. We look for activity to pick up modestly in the second half of 2019. India, other emerging markets will benefit from a pickup in Chinese growth, and a weaker U.S. dollar should translate into less risk for emerging markets this year versus 2018. Emerging market currencies did weaken in February after surging the prior month.

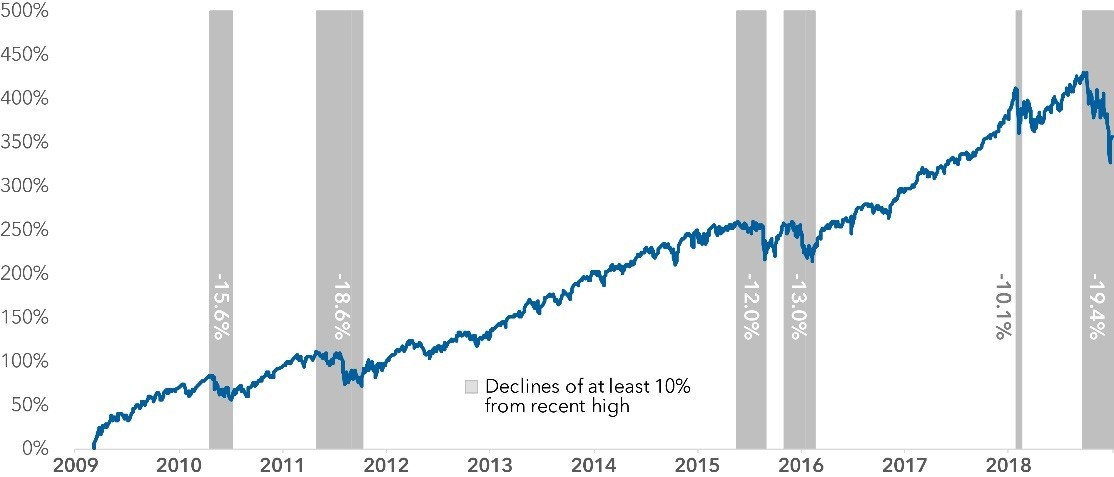

The equity market pullback from September/October 2018 was significant and in high double digits. The markets have now mostly come back since February 2019.

S&P 500 cumulative total return

Can it continue? Central banks want to unwind the decade of low interest rates. Stock and bond markets got used to that low-interest subsidy from central banks and the volatility in 2018 was the initial adjustment to that new monetary environment. In addition, world growth slowed in 2018 and the weakness persisted early this year. Markets are likely reflecting too much earnings optimism.

Further, it often takes 12 to 18 months for the full impact of central bank tightening to become apparent. So, the 2018 Fed rate hikes and bond sales have not completely worked their way through the financial system. We’d stay cautious a while longer.

Warm Regards

Aziz Meherali CFP

Six tips for autumn home improvement

With autumn here, now is the perfect time to make improvements around your home and get your property in tiptop shape for winter. Here are some ideas for the to-do list. Roof repair Small roof leaks will make it harder to keep your house warm in winter. Inspect your roof for damage (or have a ... Read more